Management accounting practices (MAPs) play a critical role in enhancing organizational performance by supporting planning, control, and strategic decision-making. This study examines the relationship between MAPs and financial performance in the context of Nepalese commercial banking, focusing on Citizens Bank International Limited (CBIL).

management accounting practices—particularly budgeting and costing—have a significant positive impact on financial performance.

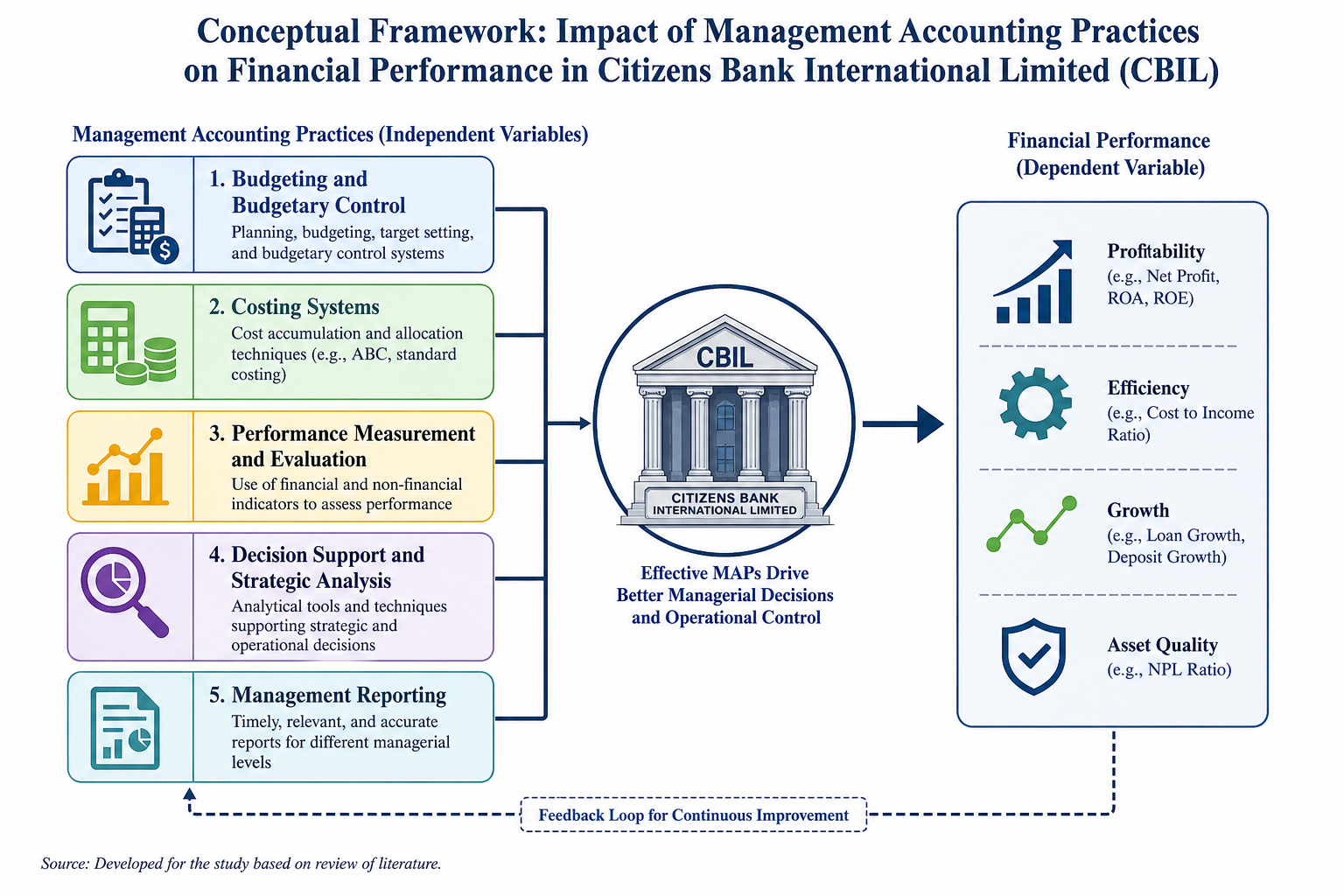

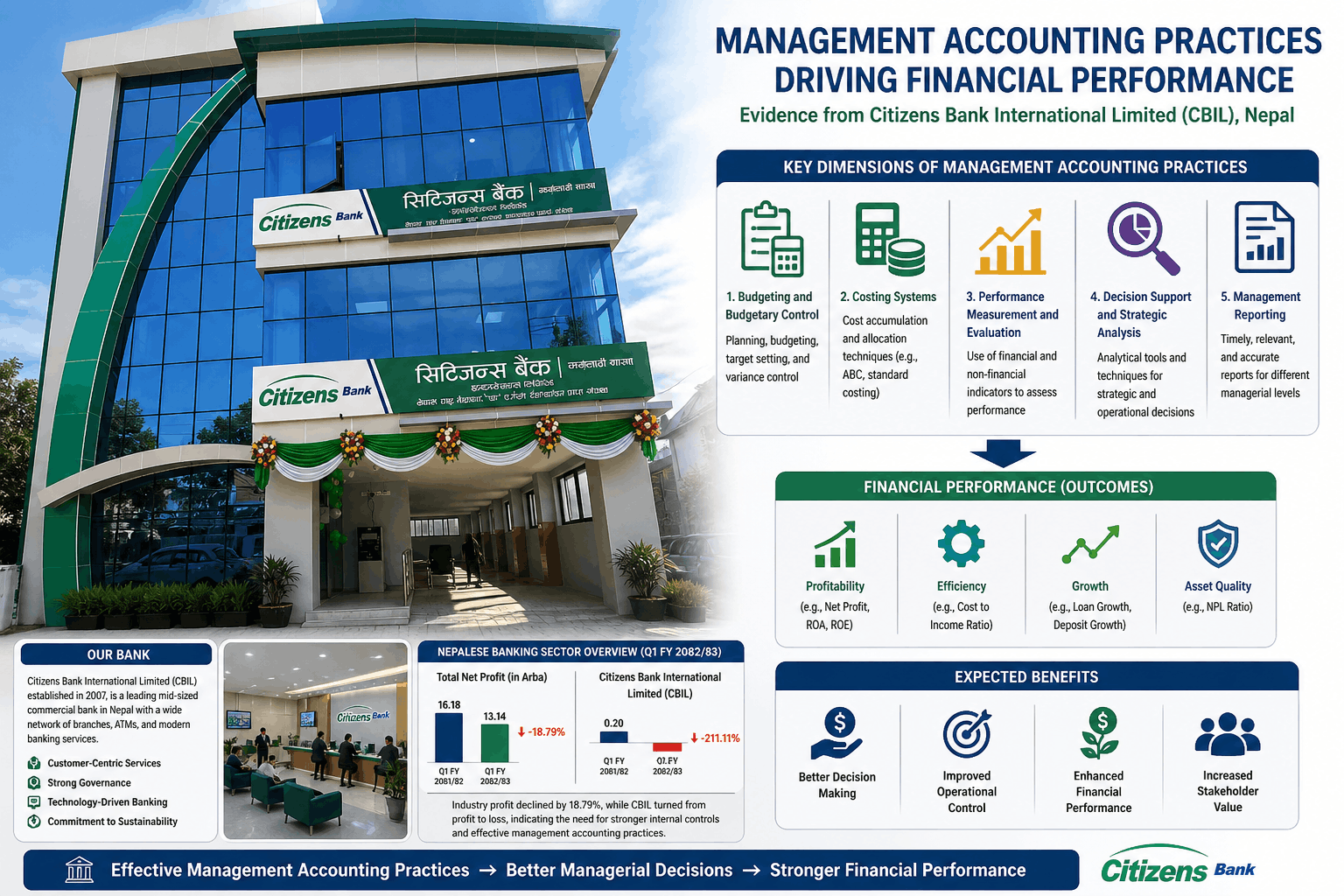

The study conceptualizes MAPs across five dimensions: budgeting and budgetary control, costing systems, performance measurement, decision support, and management reporting. Using recent financial trends within the Nepalese banking sector, the study highlights declining profitability and identifies CBIL as a critical case due to its significant performance deterioration. The findings aim to provide context-specific insights into how internal accounting systems influence financial outcomes, contributing to both academic literature and practical banking management in Nepal.

CHAPTER I

INTRODUCTION

1.1 Background of the Study

Management accounting provides internal information that supports planning, control, and decision making, and is therefore central to how organizations translate strategy into performance outcomes. Contemporary management accounting practices (MAPs) extend beyond traditional cost accumulation and variance analysis to encompass a portfolio of techniques that integrate financial and non-financial data, support strategic decision making, and facilitate performance measurement across responsibility centres (Ojra et al., 2021; Postolache, 2014). These practices include budgeting and budgetary control, costing systems such as activity-based costing, multidimensional performance measurement frameworks, decision-support analyses, and structured management reporting systems that deliver timely information to different managerial levels (Bhattarai et al., 2025; Cadez & Guilding, as cited in Ojra et al., 2021).

The banking sector represents a context in which MAPs are particularly consequential. Banks operate with high financial leverage, are tightly regulated, and are exposed to credit, liquidity, market, and operational risks. Effective internal information systems are therefore indispensable for monitoring risk-return trade-offs, maintaining cost discipline, and supporting strategic positioning within a competitive market (Postolache, 2014). Empirical work across countries indicates that banks that use comprehensive budgeting systems, rigorous performance measurement, and sophisticated costing tools tend to exhibit stronger performance and more disciplined resource allocation (Bhattarai et al., 2025; Njoki, 2016). At the same time, digitalization, the spread of financial technologies, and changing customer expectations have increased the informational demands placed on bank managers, making robust MAPs a prerequisite for timely and evidence-based decisions (Nallakaruppan et al., 2024; Raza & Tursoy, 2024).

In Nepal, commercial banks are expanding their branch networks and product portfolios while facing pressures from regulatory reforms, technological innovation, and evolving environmental and social expectations, for example, through green banking initiatives (Bhattarai et al., 2025; Thapa et al., 2025). Within this landscape, Citizen Bank International Limited (CBIL), established in 2007 and operating a large branch network across Nepal, has emerged as a significant mid-sized player in the domestic banking industry (Devex, 2025). Sustaining sound financial performance in such an environment requires not only compliance with prudential norms but also internal systems that enable managers at head office and branch levels to plan, control, and evaluate operations effectively.

Despite the theoretical and empirical importance of MAPs, there is limited systematic evidence on how specific dimensions of management accounting are configured within individual Nepalese banks and how these practices relate to concrete financial outcomes. Prior international research suggests that greater use and sophistication of MAPs are often associated with improved profitability, efficiency, and value creation, sometimes through the mediating role of more rational managerial decisions (Begum & Rahman, 2024, 2025; Gomes et al., 2013; Oyeyemi et al., 2025). However, other studies caution that the benefits of strategic management accounting are contingent on organizational context, implementation quality, and the alignment between accounting systems and strategy (Ojra et al., 2021; Oyewo & Ajibolade, 2019). These mixed findings underscore the need for context-specific investigation rather than if global patterns automatically apply to Nepalese banks.

Table 1

Net profit and year-on-year growth of selected commercial banks in Nepal (Q1 FY 2082/83 vs. Q1 FY 2081/82; amounts in Arba)

| S. No | Commercial bank | Symbol | Net profit Q1 82/83 | Net profit Q1 81/82 | Growth (%) |

| 1 | Global IME Bank | GBIME | 1.86 | 1.51 | 22.88 |

| 2 | Nabil Bank | NABIL | 1.76 | 2.06 | −14.59 |

| 3 | Prime Commercial Bank | PCBL | 1.26 | 1.29 | −2.18 |

| 4 | Everest Bank | EBL | 1.18 | 1.13 | 4.61 |

| 5 | Kumari Bank | KBL | 1.06 | 1.08 | −2.04 |

| 6 | NMB Bank | NMB | 0.92 | 1.15 | −20.09 |

| 7 | Himalayan Bank | HBL | 0.70 | 0.73 | −3.31 |

| 8 | Standard Chartered Bank | SCB | 0.69 | 0.86 | −19.72 |

| 9 | Rastriya Banijya Bank | RBBL | 0.60 | 0.15 | 295.24 |

| 10 | Nepal Bank | NBL | 0.59 | 0.60 | −2.33 |

| 11 | Prabhu Bank | PRVU | 0.56 | 1.04 | −46.35 |

| 12 | Nepal SBI Bank | SBI | 0.50 | 0.81 | −38.45 |

| 13 | Sanima Bank | SANIMA | 0.45 | 0.40 | 13.78 |

| 14 | Machhapuchchhre Bank | MBL | 0.42 | 0.50 | −17.10 |

| 15 | Laxmi Sunrise Bank | LSL | 0.33 | 0.54 | −38.06 |

| 16 | Siddhartha Bank | SBL | 0.32 | 0.38 | −15.18 |

| 17 | NIC Asia Bank | NICA | 0.12 | 0.11 | 10.91 |

| 18 | Nepal Investment Mega Bank | NIMB | 0.05 | 1.46 | −96.93 |

| 19 | Agriculture Development Bank | ADBL | 0.0057 | 0.19 | −97.00 |

| 20 | Citizens Bank International | CZBIL | −0.22 | 0.20 | −211.11 |

| Total | 13.14 | 16.18 | −18.79 | ||

| Industry average | 0.66 | 0.81 |

Source: Compiled from published Q1 FY 2082/83 and Q1 FY 2081/82 financial reports of selected commercial banks in Nepal. (Ssharesansar, 2025)

In aggregate, Table 1.1 indicates that the Nepalese commercial banking sector experienced a contraction in profitability between Q1 FY 2081/82 and Q1 FY 2082/83, with total net profit declining from NPR 16.18 Arba to NPR 13.14 Arba, equivalent to an industry-wide fall of about 18.79 percent. Although several banks such as Global IME Bank, Rastriya Banijya Bank, and Sanima Bank reported positive profit growth, many others showed substantial declines, reflecting a challenging operating environment. Citizens Bank International (CZBIL) is a conspicuous outlier: it moved from a modest profit of NPR 0.20 Arba in Q1 FY 2081/82 to a net loss of NPR 0.22 Arba in Q1 FY 2082/83, implying a sharp negative swing of approximately 211 percent. This deterioration is markedly worse than the industry total and positions CZBIL at the bottom of the profit-growth ranking. Such underperformance relative to peers underscores the urgency of examining internal determinants of financial results, including the adequacy and effectiveness of management accounting practices in planning, controlling, and supporting decisions across the bank.

The present study therefore, focuses on CBIL and conceptualizes MAPs along five core dimensions that are particularly relevant for banking: budgeting and budgetary control, costing systems, performance measurement and evaluation, decision support and strategic analysis, and management reporting. As depicted in the conceptual framework of the study (Figure 1), these five dimensions constitute independent variables, while financial performance, proxied by indicators such as profitability, efficiency, growth, and asset quality, constitutes the dependent variable. The central idea is that the design and intensity of MAPs shape the quality of managerial decisions and the degree of control over operations, which in turn should be reflected in the bank’s financial results.

YOUR COMMENT